- Equity Mates: Get Started

- Posts

- 🌱 The Get Started Investing email is back! Introducing 'How I Got Started'

🌱 The Get Started Investing email is back! Introducing 'How I Got Started'

Burned by an IPO, Saved by ETFs | How this 27-year old invests

Equity Mates

March 17, 2026

The Get Started Investing email is back!

Up until early 2024 we were sharing weekly insights every Tuesday to help you get started investing or take the next step on your journey.

Life got busy, our content schedule filled and this email was put on pause. But we’re excited to say that the Get Started Investing email is back!

Each Tuesday afternoon, we’ll share how one member of the Equity Mates community got started investing as well as one investing insight to help you understand the world of investing.

First up, one of our Research Analysts here at Equity Mates, Ned, is sharing how he got started.

Enjoy!

Bryce & Ren

Get Started Snapshot

Name: Ned “Beef Stew” Stewart

Age: 27

Hometown & current home: Melbourne/Canberra & currently living in Sydney

Profession: Research Analyst at Equity Mates Media

Favourite book: Shantaram by Gregory David Roberts

Most extravagant purchase: In 2020, I spent US$750 (around AUD$1,000 at the time) on a pair of Nike shoes I’d wanted for ages but could never justify. Then JobKeeper arrived and I suddenly had an extra $1,500 a fortnight… thanks ScoMo.

Favourite money-saving hack: Riding my e-bike to work. Upfront cost, but saving $40+ a week on public transport has more than made up for it.

What was your relationship with money like growing up?

I didn’t have much of a relationship with money growing up, which in a way was a blessing. I was never pressured to get a job early and had pretty simple tastes, so I didn’t need much pocket money.

Neither of my parents worked in finance or had much exposure to investing, so it wasn’t really discussed at home. I do remember having a CommBank Dollarmites account like most Aussie kids, that was probably my first introduction to saving.

What was your first job? (And how much did you get paid?)

My first job was picking up golf balls at Federal Golf Club in Canberra on Friday afternoons. Unfortunately, the buggy didn’t have one of those fancy ball-collecting attachments, so I had to use a handheld picker the entire time (whilst members were still hitting balls).

I got paid $15 cash for two hours of work. Not sure it would pass minimum wage laws today… or even back then.

How did you first come across investing?

Like many young Aussies, I discovered investing during COVID when I had way too much time on my hands and an extra $1,500 a fortnight from JobKeeper.

I haven’t been paid to say this (although shouting me a coffee for the plug would be nice), but Equity Mates was my first real exposure to investing. Hearing two guys who were relatable to me talk through their journey made it feel accessible and achievable.

Was there a memorable early investment?

I had a few shockers early on. The most memorable was buying Airtasker in its 2021 IPO. I used the platform when moving share houses and thought, “Great company, it must be a great investment.”

It listed around $1.40 and then dropped pretty quickly. I think I sold it a year later when it was around $0.26 so took a decent hit on that one!

That experience taught me there’s far more to investing than just liking a product. It pushed me toward ETFs, and taught me that I’m more interested in preserving and steadily growing my money than chasing a 100-bagger.

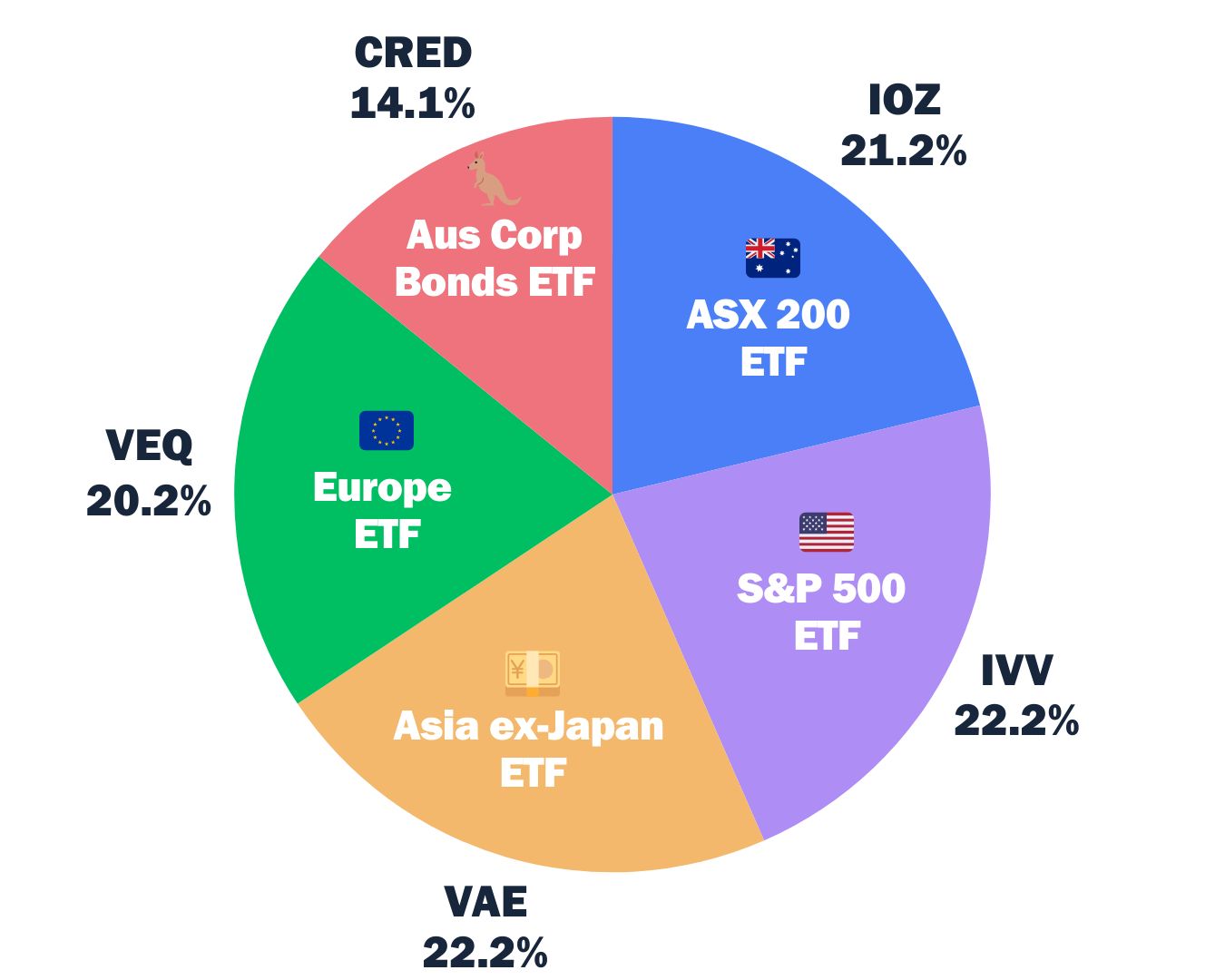

How are you currently investing and can you provide a breakdown of your portfolio?

At the moment, I aim to invest between $1,000 and $1,500 each month into five ETFs. Some months that dips if I’ve travelled or spent a bit too freely with friends.

Here’s the breakdown:

I don’t really invest in individual stocks anymore. I don’t feel I have the time or energy to consistently outperform an index and I’m more than comfortable with the returns an index can provide.

Where do you see investing taking you?

I see investing as a tool to give me flexibility in life. Not necessarily to stop working, I get a lot of purpose from work, but to have more choice later on in life would be nice.

I’d love to keep travelling with friends (and hopefully a future family), taking on new experiences, and maybe even running a few more marathons along the way (but only if it’s a super flat course and overcast like Melbourne).

If you only had 25 words to convince someone to invest, what would you say?

Investing isn’t as complicated as it may seem.

It really can be as simple or complex as you want (I prefer simple).

Your future self (and family) will thank you.

We want to hear your ‘How I Got Started’ stories. Respond to this email if you would like to be featured and we’ll get in touch!

Read a free sample of our book

Winner of the Best Personal Finance and Investment Book at the Australian Business Book Awards 2024, Don’t Stress, Just Invest gives you the simplest blueprint for investing success.

In 4 steps, we unpack the platforms to use, the investments to buy and how you can automate it all so you can set up your investments and get on with your life.

Read the opening chapter of the book for free at the link below.

How dollar cost averaging works

As Ned spoke about in his Get Started Story, using the power of dollar cost averaging to eliminate the stress and energy required to time the market can be very effective. We spoke about dollar cost averaging in our recent Get Started Investing episode titled ‘11. Tips for buying and selling’ (Spotify | Apple | YouTube)

Bryce: Let’s just explain the term quickly before we continue, Dollar Cost Averaging is simply taking the same amount of money and investing it into the market at the same cadence over a long period of time. So we all actually do it whether we know it or not through our superannuation. In the case of superannuation, it's taking 12% of your salary and investing it every time your employer pays you. So that might be every fortnight, every month, whatever it is. It's the same amount going in at the same rate

So what it's doing is you're taking out any form of guessing here or trying to time the market. It doesn't matter if it's up, if it's down, you are investing the same amount. What you're getting by doing that is when prices are low, you're buying more of it, and then when prices are high, you're buying less of the share or ETF.

Ren: So let’s see how that works in an example. If we invest $500 a month into an ETF in January, the price for that ETF is $50, so I'm going to get 10 units.

In February, it drops to $25. I'm still investing $500, but this month I'm going to get 20 units.

In March it recovers back to $50 and I get 10 units again. So what I've done there is invested $500 every month, a total of $1500. I own 40 units in total at an average price of $37.50. And that's because as it's moved up and down, I'm investing the same amount and I'm averaging out the price at which I'm buying it. So very simple, but very effective way of putting money into the market as you're getting paid every month or every fortnight and not having to worry about trying to time it.